You did everything right. You registered your LLC, you opened a dedicated business bank account, and your client just paid your first massive invoice. The money is sitting safely in your business checking account.

Now, you have to buy groceries and pay your personal rent. So… how do you actually get that money out of the business and into your pocket without angering the IRS or breaking your LLC’s legal shield?

For a 1099 freelancer, learning how to pay yourself as an LLC generally comes down to two specific methods: the Owner’s Draw or the S-Corp Salary. Here is the exact 2026 breakdown of how to move your money legally and avoid paying too much in taxes.

- Two Legal Methods Exist: Most LLC owners pay themselves via an Owner’s Draw (simple transfer) or, once profitable enough, through an S-Corp salary + distribution structure that slashes self-employment tax.

- Owner’s Draw Is Dead Simple: As a Single-Member LLC, you simply transfer money from your business account to your personal account. No payroll, no W-2 required. But taxes are not withheld—you must handle those yourself quarterly.

- The S-Corp Saves Serious Money at $60K–$80K+ Profit: By splitting income into a salary (subject to SE tax) and a distribution (exempt from SE tax), high earners can save $5,000–$10,000+ per year in self-employment taxes alone.

- Never Commingle Funds: Always transfer money to your personal account before spending it personally. Using your business debit card for groceries is a legal liability that can pierce your LLC’s liability shield.

- Reserve 25–30% for Taxes: When you take an Owner’s Draw, taxes have NOT been withheld. Always keep a tax reserve sitting in your business account to cover your quarterly estimated payments.

In This Guide

- How LLC Taxes Work (The Foundation)

- Method 1: The Owner’s Draw (For Most Freelancers)

- The Quarterly Tax Warning You Cannot Ignore

- Method 2: The S-Corp Election (For High Earners)

- The S-Corp Savings Example: $100K Profit

- The #1 Rule: Never Commingle Funds

- Which Method Should You Use? (The Final Verdict)

- Frequently Asked Questions (FAQ)

How LLC Taxes Work (The Foundation)

Before you can understand how to pay yourself as an LLC, you need to understand one fundamental concept: the IRS does not recognize the LLC as its own tax entity. Unlike a C-Corporation, which files its own separate tax return and gets taxed at the corporate level, a standard Single-Member LLC is what the IRS calls a “disregarded entity.” In plain English, the IRS looks right through your LLC and treats you and your business as the exact same taxpayer.

This means your LLC’s profits flow directly onto your personal tax return via Schedule C (Profit or Loss from Business). You pay income tax on your net profit, and you also pay the infamous 15.3% self-employment tax—which covers Social Security and Medicare—on that same profit. This is the baseline reality for most new freelance LLCs, and it informs everything about how you legally take money out of the business.

According to the IRS’s official LLC guidance, a single-member LLC is by default classified as a disregarded entity, though owners can elect to be taxed differently once their income makes it advantageous. Understanding where you start—as a disregarded entity—makes both payment methods below immediately clear.

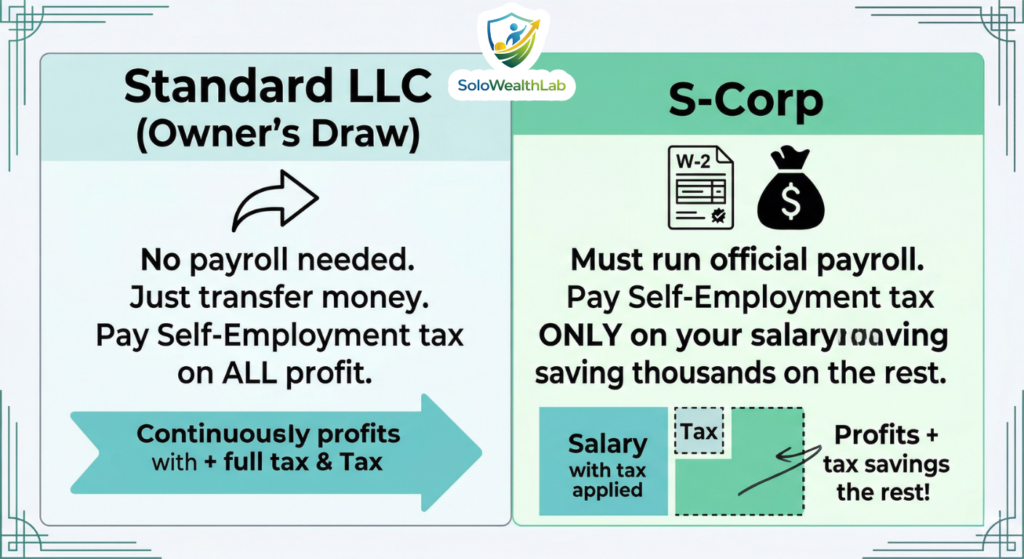

Method 1: The Owner’s Draw (For Most Freelancers)

If you are a Sole Proprietor or a standard Single-Member LLC, the IRS considers you and your business to be the same tax entity. This makes paying yourself as an LLC incredibly easy.

You do not need to run a formal payroll. You do not need to issue yourself a W-2. You do not need to file any special forms. You simply take an Owner’s Draw.

- How to do it: Log into your business bank account, click “Transfer,” and move the money directly to your personal checking account. You can also write a check from your business to yourself. That is it. The entire process takes about 90 seconds.

- How often should you do it? As often as you need to. Some freelancers take a draw once a month like a self-imposed paycheck. Others take draws whenever a large invoice clears. There is no IRS rule about frequency—you are the owner, and you can move the money whenever it makes sense for your cash flow.

- The Tax Catch: You are taxed on the total profit of your business, regardless of how much you actually transfer out to yourself. If your business profits $50,000 for the year but you only take a $30,000 Owner’s Draw, you still pay income tax and self-employment tax on the full $50,000. The draw itself is not a deductible expense—it is simply you accessing money that already belongs to you as the owner.

- What about bookkeeping? In your bookkeeping software, an Owner’s Draw is categorized as an “Owner’s Equity” transaction—not as a business expense. Tools like QuickBooks, Wave, or HoneyBook all have a specific category for this. Using the correct category keeps your profit and loss statement accurate so you always know your true business profitability.

For most freelancers who are just starting out and earning under $60,000 in net profit, the Owner’s Draw method is the correct choice. It is simple, flexible, and costs you nothing to implement. The only thing you must master alongside it is the quarterly estimated tax system—which we cover in the next section.

The Quarterly Tax Warning You Cannot Ignore

This is the most common and most expensive mistake that new LLC owners make, and it always results in a brutal surprise at tax time. Here is the danger: when you take an Owner’s Draw, no taxes have been withheld from that money. There is no employer automatically pulling out 22% for the IRS on your behalf. You are the employer and the employee—which means the responsibility is 100% yours.

Never empty your business bank account with an Owner’s Draw! Remember, when you transfer that money to your personal account, taxes have NOT been taken out yet. Always leave roughly 25% to 30% of your profits sitting in the business account so you can easily pay the IRS each quarter. Read our full Guide to Quarterly Estimated Taxes if you need the exact math on what to set aside.

The IRS requires self-employed individuals to pay their taxes in four installments throughout the year—not one lump sum in April. Missing these quarterly deadlines results in a penalty from the IRS, regardless of whether you pay your full annual tax bill correctly in April. The four deadlines for the 2026 tax year are typically mid-April, mid-June, mid-September, and mid-January of the following year.

The simplest system that works: every time a client pays you, immediately transfer 27% to 30% of that payment into a dedicated tax savings account—a separate business savings account you never touch except to make quarterly IRS payments. Think of it as the IRS’s money that is temporarily sitting in your account. Treating it that way from day one eliminates April tax surprises entirely.

Method 2: The S-Corp Election (For High Earners)

When your freelance business starts making serious money—typically around $60,000 to $80,000 in net profit per year—taking Owner’s Draws becomes increasingly expensive because you are paying the 15.3% self-employment tax on every single dollar of profit. This is where the second method for how to pay yourself as an LLC becomes extremely powerful.

To unlock this strategy, you file IRS Form 2553 to have your LLC taxed as an S-Corporation. This does not change your LLC’s legal structure or state registration—it is purely a federal tax election that changes how the IRS taxes your business income. Here is how paying yourself changes under the S-Corp structure:

- The W-2 Salary: As an S-Corp, you are now legally classified as an employee of your own business. The IRS requires you to pay yourself a “reasonable compensation” salary via official W-2 payroll—typically using payroll software like Gusto or ADP. This salary is subject to the 15.3% self-employment tax (split between employer and employee portions), federal income tax withholding, and any applicable state income tax.

- The Shareholder Distribution: Here is where the magic happens. Whatever net profit remains in the business after your W-2 salary is paid can be taken out as a Shareholder Distribution. Distributions are completely exempt from the 15.3% self-employment tax. They pass through to your personal return and are subject to income tax only—not the additional SE tax layer.

- The “Reasonable Salary” Requirement: The IRS scrutinizes S-Corps specifically because of this tax advantage. They require that your W-2 salary reflects what you would pay a market-rate employee to perform your role. Setting your salary artificially low (say, $10,000 when you are billing $200,000 as a freelance consultant) is a known IRS audit trigger. The general rule of thumb is a roughly 60/40 split between salary and distributions as a starting point, adjusted based on your industry and role.

- The Added Complexity: Running an S-Corp requires more administration than a simple Owner’s Draw. You will need payroll software to process your own W-2 paycheck, you will receive a W-2 from your own business at year-end, and you will likely need a CPA to file your additional Form 1120-S business return. These costs typically run $500 to $2,000 per year—which is why the S-Corp election only makes financial sense once your tax savings exceed those administration costs.

The S-Corp Savings Example: $100K Profit

Let us make the math real with a concrete example. Imagine your LLC generates $100,000 in net profit in 2026.

As a Standard Single-Member LLC (Owner’s Draw method):

You pay 15.3% self-employment tax on the full $100,000 (technically 92.35% of it, after the SE tax deduction), which works out to roughly $14,130 in self-employment tax alone—before income taxes.

As an S-Corp (Salary + Distribution method):

You pay yourself a $50,000 salary. The 15.3% SE tax applies only to that $50,000, resulting in roughly $7,065 in payroll taxes. The remaining $50,000 is taken as a distribution, which is exempt from SE tax entirely. You pay income tax on both amounts, but the additional SE tax layer only hits the salary portion.

Your annual savings: approximately $7,065. Over five years, that is over $35,000 in extra money you keep. The accountant’s fees to manage your S-Corp—typically $800 to $1,500 per year—are easily absorbed by those savings, making the S-Corp election one of the highest-ROI financial decisions for any high-earning freelancer.

To be taxed as an S-Corp for the current tax year, you generally need to file IRS Form 2553 within 75 days of forming your LLC, or by March 15th of the tax year in which you want the election to take effect. If you miss the deadline, the election will apply to the following year. Talk to a CPA now if you are approaching the $75,000+ profit mark—do not wait until January.

The #1 Rule: Never Commingle Funds

Whether you use an Owner’s Draw or an S-Corp structure, there is a single golden rule that governs all of LLC ownership: you must maintain a clean, documented wall between your personal and business finances at all times.

Never use your business debit card to buy personal groceries. Never use your personal credit card to pay a business vendor and then “forget” to reimburse yourself. Never pay your personal Netflix subscription from the business account. This practice is called “commingling” funds, and it is one of the most dangerous mistakes an LLC owner can make—not for tax reasons, but for legal ones.

Here is the risk: if a client or vendor ever sues your business, their attorney will subpoena your bank statements. If those statements show a pattern of commingling—personal and business expenses mixed together in the same account—a judge can declare that your LLC was never operated as a separate legal entity. This is called “piercing the corporate veil,” and it means the lawsuit can reach your personal assets: your savings account, your car, and your home. The entire legal protection that you formed your LLC to get is gone.

The solution is simple: always transfer money to your personal checking account first via a proper Owner’s Draw or Distribution, then use your personal funds for personal expenses. A dedicated business bank account paired with a business credit card creates the clean separation that protects your LLC’s liability shield. This is non-negotiable.

Which Method Should You Use? (The Final Verdict)

If you are just starting out, keep it simple. Remain a standard Single-Member LLC and take an Owner’s Draw whenever you need cash. Make sure every transfer comes from a dedicated business bank account into your personal account, and religiously set aside 25% to 30% of every payment for quarterly estimated taxes. This method requires zero setup costs, zero payroll software, and zero additional tax filings. It is the right tool for where you are right now.

Once you are consistently generating $75,000 or more in annual net profit after business expenses, schedule a meeting with a CPA—not a general accountant, but a CPA who specifically works with self-employed individuals and S-Corps. Have them run the numbers for your specific situation, industry, and state tax obligations. If the math works out (and at $75K+, it almost always does), file Form 2553, set up payroll through Gusto, and start taking Shareholder Distributions. The tax savings will pay for your accountant’s fees several times over.

Learning how to pay yourself as an LLC is not complicated once you understand the two methods and the single rule that governs both. Separate your money, set aside your taxes, and scale up to the S-Corp structure when your profits make it worth it. Every dollar you save on taxes is a dollar that goes back into building the freelance business—and financial life—you actually want.

Frequently Asked Questions (FAQ)

How do I pay myself as a single-member LLC?

As a single-member LLC, you pay yourself by taking an Owner’s Draw. Simply log into your business bank account and transfer money to your personal checking account. There is no payroll required, no W-2 to issue, and no special IRS forms to file. You are taxed on your total business profit—not on the draw amount—so always keep 25% to 30% in your business account to cover quarterly estimated tax payments.

How much of my LLC profits should I pay myself?

Most financial advisors recommend drawing no more than 50% to 70% of your net profit, especially in the early years. Reserve at least 25% to 30% for quarterly IRS tax payments and hold another 10% to 20% as a business emergency fund for slow months or unexpected costs. Once your income is stable, a CPA can help you determine the exact right draw amount based on your tax bracket, family situation, and business growth goals.

When does it make sense to elect S-Corp status for my LLC?

Most CPAs recommend electing S-Corp status when your LLC generates $60,000 to $80,000 or more in annual net profit. Below that threshold, the cost of running payroll and filing the additional Form 1120-S typically outweighs the self-employment tax savings. Above $75,000 in profit, the SE tax savings on distributions almost always exceed the S-Corp administration costs—making the election a clear financial win that usually pays for itself several times over.

Is an Owner’s Draw considered taxable income?

The draw itself is not directly taxed—your total business profit is. As a single-member LLC, the IRS taxes you on 100% of your net business profit regardless of how much you actually withdrew. If your LLC earns $60,000 but you only draw $40,000, you still owe income tax and self-employment tax on the full $60,000. The draw is simply you accessing money that already belongs to you as the business owner.

Do I need a separate business bank account to pay myself as an LLC?

Yes—a dedicated business bank account is legally essential for LLC owners, not just a best practice. Commingling business and personal funds can allow a court to “pierce the corporate veil” and expose your personal assets to business lawsuits. A separate account also makes it simple to track income, calculate draws correctly, set aside your tax reserves, and give your accountant clean records at year-end.

What is the difference between an Owner’s Draw and an S-Corp distribution?

An Owner’s Draw is taken by a standard Single-Member LLC owner as a withdrawal of their personal equity—no payroll needed, and the entire business profit is still taxed regardless. An S-Corp distribution is taken by a shareholder in an S-Corp and is specifically exempt from the 15.3% self-employment tax, making it far more tax-efficient for high earners. The critical difference: S-Corp owners must also pay themselves a reasonable W-2 salary alongside distributions, while standard LLC owners have no such requirement.