Every time you swipe your business credit card for a software subscription, a tank of gas to meet a client, or a new laptop, you are quietly lowering your tax bill.

As a 1099 freelancer, you are required to pay taxes on your net profit, not your gross revenue. This means that every legal business expense you claim directly reduces the amount of money the IRS can tax. If you make $80,000 this year but have $10,000 in deductions, you only pay taxes on $70,000.

Unfortunately, most freelancers are terrified of an IRS audit, so they leave thousands of dollars on the table by not claiming the deductions they legally deserve. Here is your ultimate 2026 cheat sheet to the absolute best 1099 tax deductions for freelancers.

- You Are Taxed on Net Profit, Not Revenue: Every legitimate business expense you deduct directly shrinks the income the IRS is allowed to tax, putting real money back in your pocket at filing time.

- The Home Office Deduction Is Legitimate: A dedicated workspace used exclusively for business qualifies for a deduction worth up to $1,500 using the simplified method—with zero receipts required.

- The 2026 Mileage Rate Is 72.5 Cents Per Mile: Driving 5,000 miles for client meetings or supply runs equals a $3,625 deduction. A mileage tracking app makes this completely effortless.

- The QBI Deduction Is Your Biggest Perk: Most 1099 freelancers qualify to deduct up to 20% of their net business income right off the top of their federal tax return—automatically calculated by your tax software.

- Organization Is Everything: The IRS requires receipts for expenses over $75. A dedicated business credit card and a Google Drive folder for digital receipts is the minimum viable recordkeeping system every freelancer needs.

In This Guide

- How 1099 Tax Deductions Actually Work

- 1. The Home Office Deduction (The Big One)

- 2. Vehicle and Mileage (The 2026 IRS Rate)

- 3. The Tech Stack (Software, Phone, & Internet)

- 4. Professional Services & Education

- 5. Self-Employed Health Insurance Premiums

- 6. The Self-Employed Retirement Deduction

- 7. The “Secret” Bonus: The 20% QBI Deduction

- The Golden Rule of Deductions

- Frequently Asked Questions (FAQ)

How 1099 Tax Deductions Actually Work

Before we dive into the list, it is worth taking sixty seconds to understand the mechanics so that you can confidently claim every dollar you are owed. As a self-employed freelancer, you report your income and business expenses on Schedule C (Profit or Loss from Business) when you file your federal tax return. The IRS subtracts your total allowable business expenses from your gross freelance revenue to arrive at your net profit. That net profit—not your total invoices—is the number your income tax and your self-employment tax are calculated from.

According to the IRS Self-Employed Individuals Tax Center, a business expense is deductible if it is both ordinary (common and accepted in your field) and necessary (helpful and appropriate for your business). You do not need to prove that an expense was absolutely required—only that it was a reasonable, legitimate cost of running your operation. With that framework in mind, here is exactly what you should be deducting in 2026.

1. The Home Office Deduction (The Big One)

If you work from your living room couch occasionally, you cannot claim this. But if you have a dedicated space in your home or apartment used exclusively and regularly for your freelance business, the IRS allows you to write it off. The key word is “exclusively”—a desk in your bedroom that doubles as a gaming station does not qualify, but a separate room you use only for client work absolutely does.

There are two ways to claim this in 2026:

- The Simplified Method: The IRS lets you deduct $5 per square foot of your home office, up to a maximum of 300 square feet (capping out at a $1,500 deduction). This requires zero math and zero receipts—just measure your office and multiply.

- The Actual Expenses Method: If your office takes up 10% of your total home square footage, you can deduct 10% of your rent or mortgage interest, 10% of your utilities, and 10% of your internet bill. This takes more math and more documentation, but it almost always produces a significantly larger deduction for freelancers who pay above-average rent in expensive cities.

Run both calculations before you file. For freelancers in high-rent cities like New York, San Francisco, or Seattle, the Actual Expenses Method can produce a deduction three to five times larger than the simplified cap. For freelancers in lower-cost areas or with smaller dedicated offices, the Simplified Method’s speed and simplicity often wins out. Either way, this single deduction can easily save you $500 to $3,000 in taxes annually.

2. Vehicle and Mileage (The 2026 IRS Rate)

Your car is a business tool. Every mile you drive to meet a client, deliver a project, attend a networking event, pick up business supplies at an office supply store, or travel to the airport for a conference directly qualifies as a business expense. The one trip you cannot deduct is your daily commute from home to a fixed regular workplace—but since most freelancers work from home, this rule rarely applies.

- The 2026 Standard Mileage Rate: For the 2026 tax year, the IRS raised the standard mileage rate to 72.5 cents per mile for business use. This rate already accounts for gas, depreciation, insurance, and maintenance—so you never need to save a single gas receipt if you use the standard rate.

- The Math: If you drive 5,000 miles for business this year, that translates into a $3,625 tax deduction from the standard mileage rate alone. If you drive 10,000 miles, that is a $7,250 write-off. Use a mileage tracking app like MileIQ, Everlance, or Hurdlr to log trips automatically every time you start driving.

- The Alternative—Actual Vehicle Expenses: Instead of the mileage rate, you can deduct the actual, documented costs of operating your vehicle for business use: gas, oil changes, tires, insurance, registration fees, and depreciation—multiplied by your business-use percentage. This method requires far more record-keeping but can produce a larger deduction if you drive a fuel-efficient car or have high depreciation on a newer vehicle.

3. The Tech Stack (Software, Phone, & Internet)

Running a digital business requires digital tools. The IRS considers these “ordinary and necessary” expenses for independent contractors, meaning they are fully or partially deductible. This is one of the easiest categories to maximize because you are already paying for most of these tools every single month.

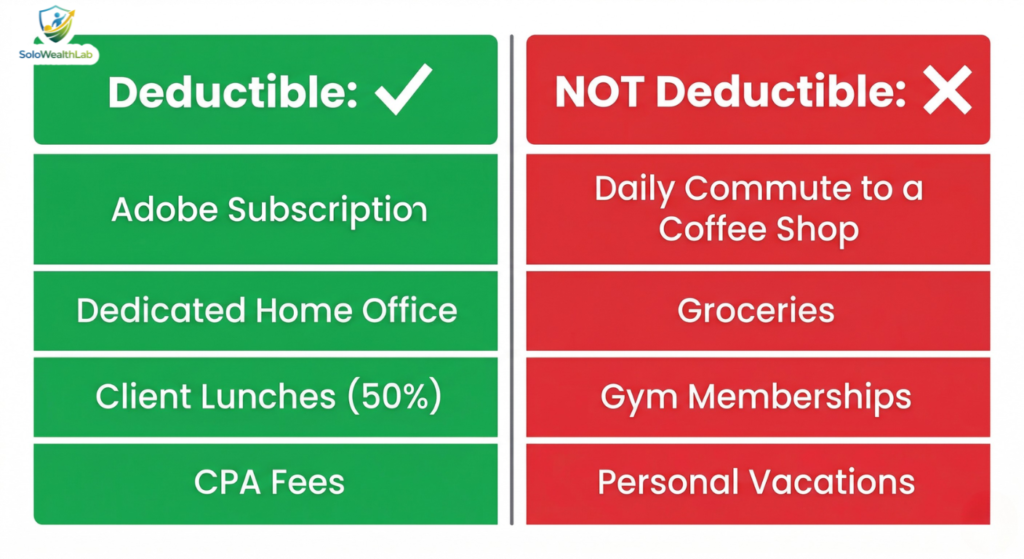

- Software Subscriptions: Your web hosting, Adobe Creative Cloud, Microsoft 365, Zoom Pro, Slack, project management tools like Asana or ClickUp, and bookkeeping software like QuickBooks, Wave, or HoneyBook are all 100% deductible business expenses.

- Hardware and Equipment: Laptops, external monitors, microphones, ring lights, keyboards, and any other equipment you purchase primarily for business use is deductible. Items costing less than $2,500 can typically be expensed in full in the year of purchase under the IRS’s de minimis safe harbor rule.

- Phone Bill: You can deduct the business-use percentage of your monthly cell phone bill. If you estimate that 60% of your calls are client calls, you can write off 60% of your Verizon, AT&T, or T-Mobile bill every month. Keep a log for one representative month to establish your business-use percentage.

- Home Internet: Similarly, if you work from home, you can deduct the business percentage of your monthly internet bill. If you use your connection roughly 70% for work, deduct 70% of your monthly ISP charge. This stacks directly on top of the home office deduction.

4. Professional Services & Education

The IRS actively rewards you for investing in your business and making sure things are done legally. Every dollar you spend to grow your skills, protect your business, or delegate work that is not your core expertise is a dollar that reduces your taxable income.

- Hiring Help: If you pay a virtual assistant, a graphic designer, a copywriter, an editor, or any other subcontractor to help deliver client work or run your business, their fees are 100% deductible. You will need to issue a Form 1099-NEC to any contractor you pay more than $600 in a calendar year, so keep detailed records of all payments made.

- Legal & Financial Fees: Did you pay a CPA or tax professional to prepare your quarterly estimated taxes or annual return? That fee is deductible. Did you pay an attorney to review a client contract, or pay LegalZoom to form your LLC? Write it off. Did you pay a financial advisor for business planning? Deductible.

- Business Education: Online courses, industry books, professional memberships, mastermind groups, podcasting subscriptions with business content, and conference tickets that directly improve your current freelance skills are all deductible. The key limitation is that the education must maintain or improve skills required in your current business—not qualify you for an entirely new career.

- Marketing and Advertising: Every dollar you spend on Facebook Ads, Google Ads, a LinkedIn Premium subscription for prospecting, your portfolio website, business cards, or hiring a photographer for professional headshots is a fully deductible marketing expense.

You cannot easily track these tax deductions if your Netflix subscription and your business software are coming out of the exact same bank account. Open a dedicated business checking account—check out our 5 Best Business Bank Accounts for Freelancers guide to find the right one—and pair it with a business credit card from our 5 Best Zero-Fee Business Credit Cards for Freelancers list. Every business purchase will be automatically logged, categorized, and ready for your accountant at tax time.

5. Self-Employed Health Insurance Premiums

This is one of the most overlooked deductions in the entire 1099 tax deductions cheat sheet, and it can be worth thousands of dollars per year. If you are self-employed and pay for your own health, dental, or vision insurance out of pocket—and you are not eligible to enroll in a subsidized health plan through a spouse’s employer—you can deduct 100% of your monthly premiums directly on your Form 1040.

Unlike most business deductions that appear on Schedule C, the self-employed health insurance deduction is an “above-the-line” adjustment to income. This means it reduces your Adjusted Gross Income (AGI) regardless of whether you itemize deductions—making it one of the most powerful and accessible deductions available to any freelancer. According to Healthcare.gov, self-employed individuals are considered their own employer for the purposes of insurance deductions, which unlocks this powerful write-off.

If you pay $600 per month for a marketplace health insurance plan, that is a $7,200 annual deduction that most employees with employer-sponsored coverage never get to take. Do not leave this one on the table.

6. The Self-Employed Retirement Deduction

Contributing to a retirement account as a freelancer does double duty: it secures your financial future and reduces your current tax bill at the same time. The IRS allows self-employed individuals to deduct contributions to several types of retirement plans, and the limits are considerably higher than what a standard W-2 employee can contribute to a 401(k).

- SEP-IRA (Simplified Employee Pension): In 2026, you can contribute up to 25% of your net self-employment income, with a maximum contribution of $70,000. Every dollar you contribute is fully deductible from your taxable income, and the account grows tax-deferred until retirement.

- Solo 401(k): If you have no full-time employees other than yourself (and a spouse), a Solo 401(k) allows you to contribute up to $23,500 as an “employee” plus an additional employer contribution of up to 25% of net self-employment income—for a potential combined total of over $70,000 per year. The entire contribution is deductible.

- SIMPLE IRA: Allows contributions up to $16,500 in 2026 with a simpler setup process, making it a strong option for newer freelancers who want to start building retirement savings immediately without the administrative overhead of a Solo 401(k).

Contributing $10,000 to a SEP-IRA does not just grow your retirement account—if you are in the 22% federal tax bracket, it immediately saves you $2,200 in federal income taxes plus reduces your state tax bill in most states. This is one of the most financially effective moves any self-employed professional can make.

7. The “Secret” Bonus: The 20% QBI Deduction

The Qualified Business Income (QBI) deduction is the holy grail for freelancers and sole proprietors, and it was introduced by the Tax Cuts and Jobs Act specifically to give self-employed individuals a tax break comparable to the corporate rate reduction that benefited larger businesses. If you qualify—and most 1099 workers do—the IRS allows you to deduct up to 20% of your net business income right off the top of your taxable income.

This means if your freelance business profits $50,000 after all your other expenses, the QBI deduction lets you subtract another $10,000 before income taxes are applied. On a $50,000 net profit in the 22% bracket, the QBI deduction alone saves you $2,200 in federal income taxes. Your CPA or tax software like TurboTax Self-Employed or H&R Block will calculate this automatically based on your income and business type.

The one important caveat: if your total taxable income exceeds approximately $197,300 (for single filers) or $394,600 (for married filing jointly) in 2026, phase-out rules and “Specified Service Trade or Business” (SSTB) limitations may begin to reduce your QBI deduction. Freelancers in fields like law, health, financial services, and consulting should verify their eligibility with a CPA once their income approaches these thresholds.

The Golden Rule of Deductions

The IRS requires you to keep receipts and documentation for any business expense over $75. But in 2026, recordkeeping does not have to be a shoebox of crumpled paper on your kitchen counter. The most organized freelancers use a dead-simple three-part system to make sure every deduction is airtight and audit-proof.

First, put every single business purchase on a dedicated business credit card or business checking account. This creates an automatic, timestamped record of every transaction without any manual effort. Second, photograph and save your digital receipts to a dedicated Google Drive or Dropbox folder organized by month. Most receipt-scanning apps like Dext or Expensify can do this automatically. Third, connect your business card and bank account to bookkeeping software like QuickBooks, Wave, or HoneyBook so that your profit and loss statement stays current all year—not just in the panicked weeks before April 15th.

The more organized your records, the more confidently you can claim every deduction you deserve, and the better positioned you are to survive an audit without a single dollar of penalties. The IRS cannot challenge what you can clearly document. Start building your recordkeeping system today—every dollar you track is a dollar that stays in your pocket at tax time.

Frequently Asked Questions (FAQ)

What is the most valuable 1099 tax deduction for freelancers?

The 20% Qualified Business Income (QBI) deduction is typically the single most valuable deduction available to 1099 freelancers. It lets most self-employed individuals deduct up to 20% of their net business income directly from their taxable income before rates are applied. The home office deduction, self-employed health insurance premiums, and retirement account contributions (SEP-IRA or Solo 401(k)) are the other highest-value deductions that most freelancers consistently underutilize.

Do I need an LLC to claim 1099 tax deductions?

No. Sole proprietors, independent contractors, and single-member LLCs all report business income and expenses on Schedule C and qualify for the exact same set of 1099 tax deductions. An LLC does not unlock any additional write-offs. The deductions are available based on your self-employment activity—not your legal entity structure—so you can claim every deduction on this cheat sheet whether you are a registered LLC or an unincorporated sole proprietor.

What is the IRS standard mileage rate for 2026?

The IRS standard mileage rate for business driving in the 2026 tax year is 72.5 cents per mile. This single rate already accounts for gas, insurance, maintenance, and vehicle depreciation, so no gas receipts are required. Simply log your business miles using a tracking app like MileIQ, Everlance, or Hurdlr, then multiply your total annual business miles by 72.5 cents to calculate your full mileage deduction at tax time.

Can I deduct my home office if I rent my apartment?

Yes, absolutely. Renters qualify for the home office deduction on exactly the same terms as homeowners. Using the Actual Expenses Method, you can deduct the percentage of your monthly rent that corresponds to the percentage of your apartment used exclusively as your home office. If your dedicated office represents 12% of your total square footage, you deduct 12% of every month’s rent as a business expense. The IRS has no requirement that you own your home to claim this deduction.

What records do I need to keep to defend my freelancer tax deductions?

The IRS requires documentation for any expense over $75. The most reliable system uses a dedicated business credit card for all purchases (creating an automatic transaction log), a cloud folder for digital receipt photos organized by month, and bookkeeping software like QuickBooks or Wave that syncs with your accounts year-round. For mileage, a tracking app replaces the need for any manual log. Bank and credit card statements alone are generally sufficient documentation for expenses under the $75 threshold.

Are software subscriptions fully deductible for freelancers?

Yes. Software subscriptions used primarily for your freelance business are considered ordinary and necessary business expenses by the IRS and are 100% deductible in the year you pay for them. This covers tools like Adobe Creative Cloud, Microsoft 365, Zoom, Slack, Asana, bookkeeping software, and web hosting. The subscription must be used primarily for business operations—not personal entertainment—to claim the full deduction without needing to prorate between personal and business use.