You landed your first client, the money is hitting your bank account, and suddenly, a wave of panic sets in. You ask yourself: “Wait, am I operating illegally? Do I need to form an LLC? What if someone sues me?”

This is the exact moment every freelancer realizes that doing the work is only half the job. The other half is protecting the wealth you are building. You have crossed the threshold from hobbyist to business owner, and your legal exposure has shifted entirely.

In the 1099 economy, there is a massive amount of confusion about legal business entities. The internet is full of conflicting advice: some creators claim you must form an LLC immediately to save on taxes, while others insist a Sole Proprietorship is completely fine for years.

Let’s strip away the legal jargon and break down exactly what a Sole Proprietorship is, what a Limited Liability Company (LLC) does, and determine whether you actually need a sole proprietor vs llc freelancer setup in 2026.

- The Default Status: You are automatically a Sole Proprietor if you freelance without filing paperwork, but your personal assets are completely exposed to lawsuits.

- The Corporate Shield: An LLC creates a legal barrier that protects your personal life savings, home, and vehicles from business debts and litigation.

- The Tax Myth: A standard single-member LLC does not magically save you money on taxes; the IRS taxes it exactly the same as a Sole Proprietorship.

- The Golden Rule: If you form an LLC, you must open a separate business bank account immediately. Co-mingling funds destroys your legal protection.

In This Guide

What is a Sole Proprietorship? (The Default Mode)

If you start driving for Uber, walking dogs on Rover, or designing logos on a freelance basis, and you file absolutely zero paperwork with your state… congratulations! You are automatically a Sole Proprietor.

A Sole Proprietorship is the default business structure in the United States. It simply means that you, as an individual, own and operate a business. There is no legal distinction between the owner and the business entity.

The Pros of Being a Sole Proprietor

- It is 100% Free to Start: There is no state paperwork to file (other than potentially a local business license or a “Doing Business As” / DBA name if you don’t use your legal name).

- Zero Annual Fees: You do not have to pay the state franchise taxes or annual business registration fees that corporations and LLCs often face.

- Incredibly Simple Taxes: You do not file a separate corporate tax return. You simply report your business income and expenses on a Schedule C attached to your personal Form 1040 tax return.

- Complete Control: You are the sole decision-maker. You don’t need to hold board meetings, record minutes, or pass corporate resolutions.

The Cons (The Danger Zone)

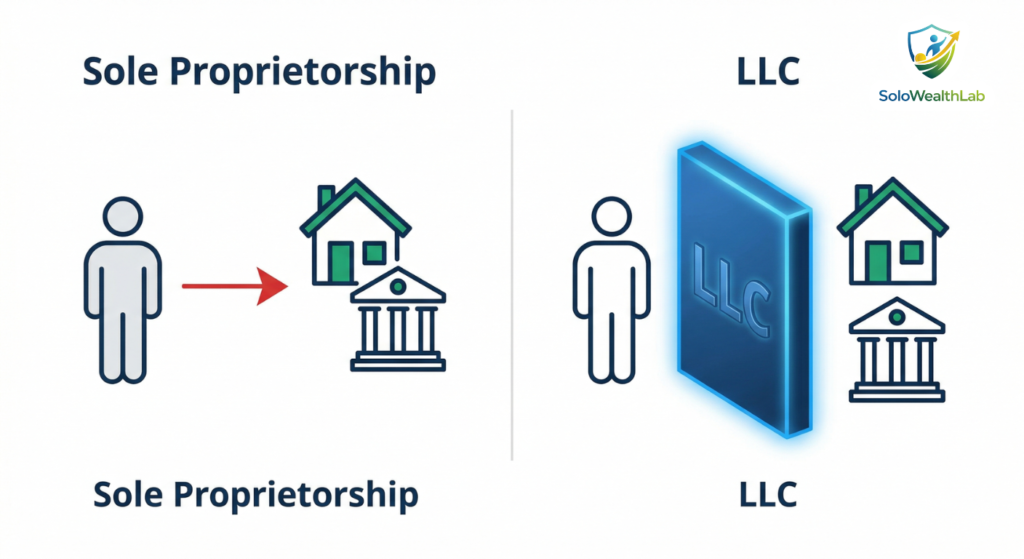

- Unlimited Personal Liability: Because the law views you and your business as the exact same entity, there is no legal shield. If your freelance business gets sued (for example, if a client claims your marketing campaign cost them $50,000, or someone trips over your camera tripod at an event), you are personally on the hook.

- Your Personal Assets are at Risk: If you rack up business debt or face a massive lawsuit judgment, creditors can come after your personal bank accounts, your car, your investments, and in some cases, your home.

- Harder to Get Business Credit: Banks perceive Sole Proprietorships as riskier. It can be significantly more difficult to secure a business credit card or a small business loan without an official legal entity.

What is an LLC? (The Corporate Shield)

A Limited Liability Company (LLC) is a formal legal business structure that you create by filing specific paperwork—usually called the Articles of Organization—with the Secretary of State where you live or operate.

Think of an LLC as an invisible legal box. You put your business operations inside the box. You remain outside the box. If someone sues the business, they are suing the box, not you directly.

The Pros of an LLC

- Personal Asset Protection: An LLC creates a legal “brick wall” (the corporate shield) between your personal life and your business. If your business is sued or goes bankrupt, the lawsuit can generally only target the assets owned by the LLC. Your personal life savings, your house, and your retirement accounts remain protected.

- Professional Credibility: Operating as “John Doe Media, LLC” looks much more professional and established to corporate clients than simply invoicing as “John Doe.” Some larger corporations even refuse to work with 1099 contractors who do not have an established LLC, purely for liability reasons.

- Flexible Tax Options: While an LLC is taxed like a Sole Proprietorship by default, you have the unique ability to tell the IRS to tax you as an S-Corporation later down the road. This flexibility can be incredibly lucrative once you hit a certain income threshold.

The Cons of an LLC

- Initial Costs: It costs money to form. Depending on your state, forming an LLC can cost anywhere from $40 (Kentucky) to $500 (Massachusetts).

- Ongoing Annual Fees: You usually have to pay an annual or biennial fee to keep your LLC active. For example, California famously charges a minimum $800 annual franchise tax just to have an LLC, regardless of whether you make a profit.

- Maintenance and Compliance: You must maintain the LLC by filing an annual report, maintaining a Registered Agent, and strictly separating your business and personal finances.

The Biggest Myth: “LLCs Save You Money on Taxes”

There is a dangerous piece of misinformation circulating online. Many freelancers rush to form an LLC because TikTok or YouTube told them it was a “tax write-off cheat code.” This is entirely false.

By default, the IRS doesn’t actually recognize an LLC as a distinct taxing entity. They consider a single-member LLC to be a “disregarded entity.”

This means that for tax purposes, a standard single-member LLC and a Sole Proprietorship are exactly the same. You still file a Schedule C on your personal tax return. You still pay your standard income tax brackets. You still pay the exact same 15.3% self-employment tax (Medicare and Social Security) on all your net profits.

Furthermore, you get the exact same tax deductions. You do not need an LLC to write off your laptop, deduct your internet bill, claim the home office deduction, or use the 72.5-cent IRS mileage rate for business driving in 2026. A Sole Proprietor has access to all of these write-offs legally.

You form an LLC primarily for legal protection, not for immediate tax savings.

When an LLC Actually Does Save You Money (The S-Corp Election)

There is one massive exception: The S-Corporation tax election.

Once your freelance business is consistently clearing above $60,000 to $80,000 in pure net profit per year, a standard LLC will result in a massive 15.3% self-employment tax bill. However, because you have an LLC, you can file IRS Form 2553 to be taxed as an S-Corp.

Under an S-Corp, you split your income. You pay yourself a “reasonable salary” (which is subject to the heavy 15.3% tax), and you take the rest of your profit as a “shareholder distribution” (which legally completely bypasses the 15.3% self-employment tax, saving you thousands).

Note: You cannot make this S-Corp election if you are just a Sole Proprietor. You must form the LLC first.

Let’s say you spend the money to form an LLC, but you continue using your personal checking account to buy business software, and you deposit client checks right next to your grocery money. In the event of a lawsuit, a judge will look at your accounts and declare that the LLC is just a “sham.” They will instantly pierce the corporate veil, completely destroying your liability shield, and allow creditors to sue you personally anyway.

If you are starting an LLC, you must open a separate, dedicated business bank account. The second you get your EIN, open the account. Check out our guide to the 5 Best Free Business Bank Accounts for Freelancers to get set up properly today.

Freelance Risk Factors: Assessing Your Need for an LLC

When analyzing the sole proprietor vs llc freelancer debate, everything comes down to your personal risk tolerance and the specific industry you operate in.

1. Low-Risk Solopreneurs

If you are a freelance writer, a remote graphic designer, a virtual assistant, or a digital illustrator, your physical risk is virtually zero. You aren’t operating heavy machinery, you aren’t rendering medical advice, and nobody is physically visiting a retail location you own.

In these cases, a Sole Proprietorship is often perfectly fine for your first few years. Your biggest risk is a client demanding a refund or claiming copyright infringement. Often, purchasing a simple, low-cost Professional Liability (Errors & Omissions) insurance policy is cheaper and more protective for these specific scenarios than managing an LLC.

2. High-Risk Independent Professionals

If you work in the physical world, your risk skyrockets. You should strongly consider forming an LLC immediately if you are a:

- Personal Trainer or Yoga Instructor: If a client tears a ligament while following your fitness routine, they may sue you for medical bills.

- Event Planner or Wedding Photographer: If your lighting equipment falls and injures a guest, or if you accidentally format the memory card containing someone’s wedding photos, the damages can be devastating.

- Handyman, Contractor, or Tradesperson: Property damage claims are common and incredibly expensive.

- Dietitian, Consultant, or Financial Coach: If a client relies on your specific advice and suffers financial or medical damages as a result.

When Should a Freelancer Actually Upgrade to an LLC?

So, do you really need one? Here is the general rule of thumb for independent contractors and freelancers navigating 2026:

- Stay a Sole Proprietor if:

- You are just testing the waters with a new side hustle.

- You are bringing in under $10,000 per year.

- You operate entirely digitally with no physical risks.

- You live in a state where LLC costs are crushingly high (like California’s $800 annual fee), and your revenue doesn’t justify the expense yet.

- Form an LLC if:

- You are operating in a high-risk physical industry.

- You have significant personal assets to protect (you own a home, have a large investment portfolio, or have a spouse with significant assets).

- You are signing massive client contracts with heavy liability clauses.

- You plan to hire subcontractors or actual W-2 employees to help you scale.

- Your net profit is approaching the $60,000+ range and you want to utilize the S-Corp tax election to save on self-employment taxes.

Want the Protection? Here is How to Form Your LLC

If you decide it is time to build that legal wall around your personal assets, the good news is that you don’t need to pay a lawyer $3,000 to file the paperwork.

Here is the streamlined process to properly establish your LLC in 2026:

- Choose a Unique Business Name: It must be distinct from any other registered business in your state and typically must end in “LLC” or “L.L.C.”

- Nominate a Registered Agent: This is a person or service that sits available during normal business hours to accept legal mail (like a lawsuit) on your behalf. Many online services will act as your Registered Agent for about $100 per year.

- File Articles of Organization: Submit this document to your Secretary of State along with the state filing fee. This officially brings your entity into existence.

- Create an Operating Agreement: This internal document outlines how the LLC is run. Even as a single-member freelance LLC, having this document on file proves your business is a legitimate, separate entity.

- Get an EIN (Employer Identification Number): This is entirely free directly from the IRS website. It acts as the Social Security Number for your business, allowing you to open a business bank account without handing out your personal SSN to clients.

Frequently Asked Questions (FAQ)

What happens if I get sued as a sole proprietor?

If you are sued as a sole proprietor, you are held personally liable. This means a court can order the seizure of your personal assets, including your personal savings accounts, your vehicle, and potentially your real estate, to satisfy the business debt or legal judgment.

Does an LLC protect me from professional negligence?

An LLC protects your personal assets from general business debts and slip-and-fall type liabilities. However, an LLC does not protect you from personal professional malpractice, negligence, or intentionally fraudulent acts (known as torts). For errors in your professional advice or services, you specifically need Errors and Omissions (E&O) or Professional Liability insurance in addition to your LLC.

Can I form an LLC in Wyoming or Delaware to save on taxes?

Many “gurus” suggest forming an LLC in states with privacy laws and zero income tax. However, for a solo freelancer, it usually defeats the purpose. If you form an LLC in Wyoming but do all your freelance work from your living room in California, California will force you to register your Wyoming LLC as a “Foreign LLC” doing business in their state. You will end up paying filing fees, registered agent fees, and franchise taxes in two different states.

Do I have to pay myself a formal salary with an LLC?

If you have a standard single-member LLC, no. You pay yourself simply by taking an “Owner’s Draw”—which means you just transfer money from your business checking account to your personal checking account. However, if your LLC has utilized the S-Corp tax election, you are legally required by the IRS to set up actual payroll and pay yourself a W-2 “reasonable salary” with regular tax withholdings.

Wrap-Up: Treat Your Freelance Hustle Like a Real Business

The choice between remaining a sole proprietor vs llc freelancer ultimately comes down to treating your operation like a legitimate business enterprise rather than just a weekend side hustle.

If the physical and financial risks in your industry are high, or if you have a significant personal net worth that you cannot afford to lose, the initial cost of filing Articles of Organization and setting up an LLC is a cheap insurance policy for your lifelong peace of mind. You can easily form an LLC online using affordable services that handle all the state paperwork and act as your Registered Agent.

Treat your business right, properly separate your bank accounts, protect your assets, and file the paperwork. You will sleep much better at night.