Let’s be honest: when you first start out as a freelancer or gig worker, retirement is usually the absolute last thing on your mind. You’re focused on landing the next client, hitting your weekly Uber earnings goal, or just figuring out how to pay your quarterly estimated taxes without draining your checking account. But eventually, your business stabilizes. You start making real money, and suddenly, a standard high-yield savings account just isn’t enough to shelter your hard-earned cash from the IRS.

When you start searching for high-limit retirement plans built specifically for the self-employed, one name consistently hits the top of the list: Fidelity Investments.

Fidelity’s “Self-Employed 401(k)” has long been considered the gold standard for solo entrepreneurs, mostly because they flat-out refuse to nickel-and-dime you with administrative fees. But the landscape of gig economy finance changes rapidly. Is Fidelity actually the right fit for your specific hustle in 2026? We’ve broken down the highly anticipated new Roth updates, the massive 2026 contribution limits, and exactly how to get your account running from your laptop in under 20 minutes.

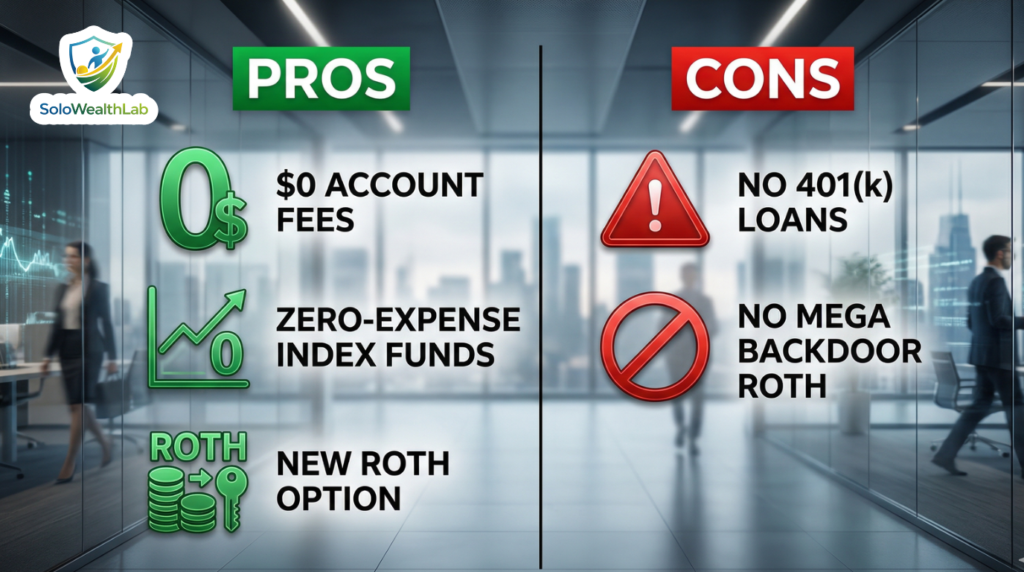

- Zero Fees: Fidelity still charges $0 for account setup, $0 for annual maintenance, and $0 for standard index fund trades.

- The Roth Game-Changer: Freelancers can now finally make after-tax Roth contributions on the platform—meaning 100% tax-free withdrawals in retirement.

- Massive Tax Shield: You can legally stash away up to $72,000 this year (plus additional catch-ups if you are over 50).

- The Drawbacks: Fidelity still does not support 401(k) participant loans or complex “Mega Backdoor” Roth strategies.

1. Fidelity Solo 401(k): The Real Pros & Cons

Fidelity is built from the ground up for the DIY investor. It is designed for the freelancer who wants to keep every single penny of their 1099 payouts working for them, rather than paying a financial advisor 1% a year in “management fees.” Here is where the platform truly shines, and where it falls slightly short of perfection.

The Pros:

- Actually Free: Many brokerages claim to be free but sneak in hidden custody fees or statement fees. Fidelity has no setup fees, no annual maintenance fees, and no minimum balance requirements. It’s incredibly rare to find a platform this robust that carries truly $0 administrative overhead.

- The “ZERO” Funds: Fidelity’s proprietary ZERO index funds (like FZROX and FZILX) charge exactly 0% in management expense ratios. It is literally the cheapest possible way to own the entire U.S. and International stock markets.

- Fractional Shares: Have exactly $142.50 left over at the end of the month after paying business expenses? You can invest every single cent into a high-priced stock or ETF using fractional shares without leaving cash sitting uninvested on the sidelines.

- New Roth Access: For years, the biggest complaint about Fidelity’s solo plan was that it only offered Traditional (pre-tax) accounts. They’ve finally updated their plan documents to allow Roth contributions! This is a massive win for younger freelancers or anyone who expects to be in a higher tax bracket later in life.

The Cons:

- No Loans Allowed: This is the biggest sticking point for many business owners. A major perk of a Solo 401(k) is that the IRS allows you to borrow up to $50,000 from your own account in an emergency. However, Fidelity’s specific plan document does not allow participant loans. If your business hits a lean month and you desperately need cash, you cannot borrow from this account without facing severe early withdrawal penalties.

- Paperwork Hurdles for Rollovers: While opening a new account is a breeze online, rolling over an old 401(k) from a previous corporate employer can still involve the dreaded “print and mail” process with physical checks. It feels a bit archaic for 2026.

2. 2026 Contribution Limits: How Much Can You Stash?

The Solo 401(k) is an absolute powerhouse of a retirement vehicle because it allows you to act as both the “Employee” and the “Employer” of your own solo business. For 2026, the combined contribution limit is a staggering $72,000. Here is how the math breaks down:

- As the Employee (Elective Deferral): You can defer up to $24,500 of your net business income. You can choose to make this contribution as Traditional (lowering your current tax bill) or Roth (tax-free later).

- As the Employer (Profit-Sharing): Your business can make a profit-sharing contribution of up to 25% of your net adjusted business income (or 20% if you are a sole proprietor). These employer contributions are always Traditional pre-tax.

When making your Employee deferrals, you face the classic debate: Traditional or Roth? Traditional contributions lower your current taxable income right now, which is fantastic if your freelance business had a blockbuster year and you need immediate tax relief. Roth contributions don’t give you a tax break today, but every dollar grows tax-free forever. For many gig workers just starting out and sitting in lower tax brackets, locking in those Roth contributions through Fidelity is an incredible wealth-building hack.

Pro Tip: If you’re age 50 or older, you get an extra $8,000 catch-up contribution. And if you fall into the new SECURE 2.0 “Super Catch-Up” window (ages 60 to 63), you can add a massive $11,250 on top of the base limits this year!

3. Best Investment Options: The “Fidelity ZERO” Strategy

One of the biggest mistakes new investors make is funding their Solo 401(k) and thinking the job is done. When your money hits the Fidelity account, it usually sits in a money market fund (a “core position”) earning decent, but relatively low, interest. To actually grow your wealth and beat inflation over decades, you must manually invest it.

Because Fidelity doesn’t charge trading commissions on standard ETFs and mutual funds, you have the entire stock market at your fingertips. However, most successful freelancers we talk to keep things incredibly simple with a “Three-Fund Portfolio” using Fidelity’s zero-fee options:

- FZROX (Fidelity ZERO Total Market Index): This fund exposes you to thousands of U.S. companies. It has a 0% expense ratio, meaning you keep all the dividends and growth instead of paying Wall Street.

- FZILX (Fidelity ZERO International Index): This gives you exposure to markets outside the U.S. (Europe, Asia, emerging markets) to keep your portfolio globally diversified, also at a 0% fee.

- FXNAX (Fidelity U.S. Bond Index Fund): While not a “ZERO” fund, the fee is a microscopic 0.025%. Adding bonds helps smooth out the wild volatility of the stock market.

By using these three funds, you can build a world-class retirement portfolio without paying a single cent in recurring management fees.

4. Fidelity vs. Vanguard vs. Schwab

Fidelity is considered one of the “Big Three” discount brokerages, but how does it stack up against its main rivals for a Solo 401(k)?

Vanguard: Vanguard has a legendary reputation among index fund investors. However, their technology and website often feel like they are stuck in 2005. More importantly, Vanguard recently offloaded their small business retirement plans to Ascensus, which means you are no longer dealing directly with Vanguard’s in-house platform for a new Solo 401(k), and new administrative fee structures may apply.

Charles Schwab: Schwab is fantastic, offers great customer service, and supports Roth Solo 401(k) options. However, Fidelity’s proprietary “ZERO” funds and superior fractional share investing capabilities give Fidelity the edge for most gig workers who are starting small and want maximum flexibility.

What about Robo-Advisors? Platforms like Betterment or Wealthfront are incredibly easy to use, but they charge an automated management fee (usually around 0.25% of your assets every single year). That might not sound like much, but over 30 years, it can eat tens of thousands of dollars of your potential growth. By taking 15 minutes to set up a Fidelity Solo 401(k) and buying zero-fee index funds yourself, you keep all of that money in your own pocket.

5. Step-by-Step: How to Open Your Account in 2026

Do not let the legal jargon scare you. Setting this up takes about 15 to 20 minutes if you have your documents ready. Here is the exact playbook:

- Get your EIN: Even if you are a “business of one” operating as a sole proprietor, you need an Employer Identification Number (EIN) to open a Solo 401(k). It is completely free and takes 5 minutes to generate on the official IRS.gov website. Never pay a third-party service to do this for you!

- Apply Online: Head directly to the Fidelity Self-Employed 401(k) page and click “Open an Account.” The digital application will walk you through naming your plan (e.g., “Jane Doe Freelance 401k Trust”).

- Open Both Account Types: During setup, we highly recommend checking the boxes to open both a Traditional and a Roth account simultaneously. It costs nothing extra and gives you the ultimate flexibility to choose where your money goes based on your tax situation at the end of the year.

- Link Your Business Bank: Once approved, log in and use Plaid to securely link your dedicated business checking account. Make your first transfer.

- Invest the Cash: Once the transfer clears, go to the trade ticket and buy your chosen index funds to put your money to work!

6. Final Verdict: Should You Use Fidelity?

If you want a strictly fee-free, “set it and forget it” retirement plan with a sleek mobile app and zero-cost index funds, Fidelity is a no-brainer. It brilliantly solves 95% of the problems freelancers face when trying to save aggressively for the future.

The only legitimate reasons to look elsewhere are if you specifically need a “Self-Directed” plan to invest in alternative assets like real estate, you desperately want the ability to take a 401(k) loan, or you are a massive high-earner hunting for a platform that explicitly supports the complex Mega Backdoor Roth strategy. For everyone else, Fidelity is the absolute king of the hill.

Ready to build your overarching wealth strategy? Check out our Ultimate Guide to Retirement Planning for Gig Workers to see how the Solo 401(k) pairs with IRAs and HSAs.

Frequently Asked Questions

Do I need to have an LLC to open this?

Nope. Whether you’re an Uber driver, a freelance writer, or a consultant, as long as you have legitimate 1099 self-employment income and an EIN, you’re good to go as a sole proprietor.

Is there a deadline to open the account?

Technically, you have until your tax filing deadline (usually April 15th of the following year) to both establish and fund the Solo 401(k) plan. However, we always recommend getting the account opened by December 31st so your bookkeeping and tax planning remain clean and stress-free.

Can I really withdraw Roth money tax-free?

Yes! That’s the beauty of the new Fidelity Roth update. You pay income taxes on the money now, but when you retire, all the compounding growth, dividends, and withdrawals are 100% tax-free under IRS rules.

Can I roll over an old W-2 401(k) into my Fidelity Solo 401(k)?

Yes, Fidelity allows you to roll over funds from a previous employer’s 401(k), 403(b), or Traditional IRA into your new Solo 401(k) to consolidate your retirement accounts. You will need to initiate a rollover request and may need to handle a physical check.

What happens if I hire an employee later?

The Solo 401(k) is strictly for businesses with no full-time employees other than yourself and your spouse. If you hire a W-2 employee who works more than 1,000 hours a year, you must convert the plan to a standard 401(k) or a SEP IRA to remain compliant with the IRS.