The #1 mistake new freelancers, 1099 contractors, and gig workers make is “Co-mingling.” This is a sophisticated tax term for simply mixing your business income with your personal grocery and rent money in a single, unorganized bank account. While it might seem easier to just have one checking account when you’re first starting out, this habit is setting a trap that could cause massive headaches down the road.

Not only does co-mingling make tax season an absolute nightmare (forcing you to sift through months of personal transactions to find your deductible expenses), but it can also put your personal assets at severe risk. If you operate as a Single-Member LLC, mixing funds can “pierce the corporate veil,” meaning if your business is ever sued, your personal savings, car, or home could be targeted. Even if you are a sole proprietor, keeping clean books is essential for taking maximum deductions and surviving a potential IRS audit.

The good news? In 2026, there is no valid excuse for mixing your money. The era of paying a traditional brick-and-mortar bank a $15 monthly fee just to host your business cash is over. Modern fintech companies and online banking platforms offer incredibly powerful, completely fee-free tools designed specifically for the dynamics of the 1099 economy.

We’ve spent hundreds of hours testing, reviewing, and comparing the top business banking solutions. Below, you will find our carefully curated guide to the 5 best free business bank accounts for freelancers. These platforms will help you automate your taxes, streamline your bookkeeping, issue professional invoices, and radically protect your solo wealth.

- Always separate personal and business funds to protect your assets (especially for LLCs) and simplify tax deductions.

- Modern fintech accounts offer zero monthly fees and no minimum balance requirements for 1099 contractors.

- Look for helpful built-in features like automated tax saving (reserves/folders), professional invoicing, and simple bookkeeping.

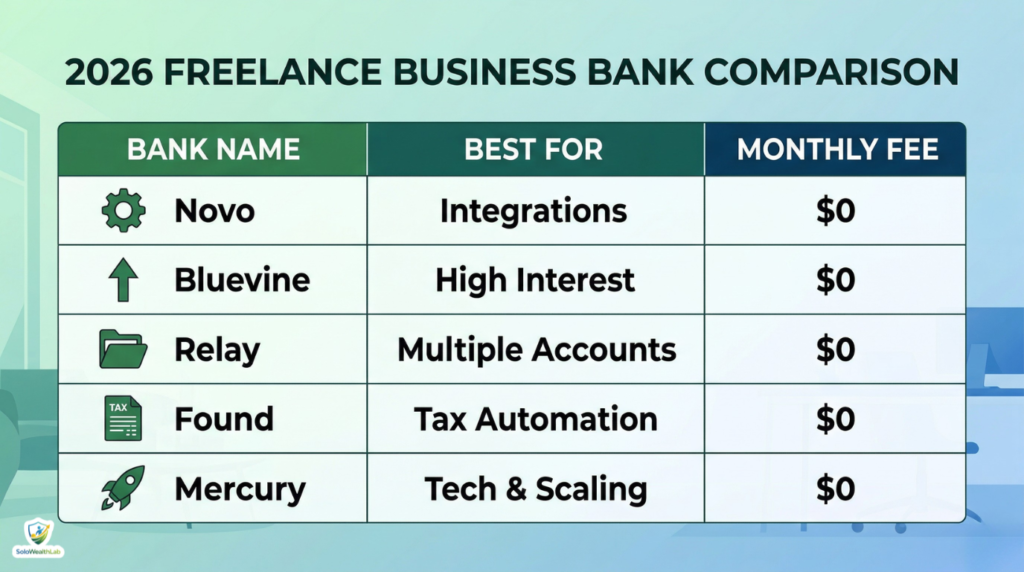

- Novo is best for seamless tool integrations, while Bluevine leads with high-yield interest options.

- You do not need an EIN to open an account; a Social Security Number is perfectly fine if you are a sole proprietor.

Why You Need a Dedicated Business Account in 2026

Before diving into the top five recommendations, let’s briefly look at why a dedicated account is non-negotiable for modern freelancers:

- Tax Compliance: Come tax time, you can easily export a CSV file of every single business transaction to hand over to your CPA or upload into software like TurboTax or QuickBooks.

- Professionalism: When clients write you a check or pay via ACH, they expect to pay “[Your Name] Consulting” or your LLC name, not your personal checking account. It elevates your brand authority.

- Automation: Modern accounts offer sub-folders and “envelopes” to automatically stash away a percentage of your income for quarterly estimated taxes.

- Financial Clarity: You can clearly see your profit margins. If your business account is growing, you’re profitable. If it’s shrinking, you need to adjust your pricing or cut expenses.

1. Novo: Best Overall for Software Integrations

Novo has firmly established itself as the gold standard for solo founders, creative freelancers, and digital nomads. Built from the ground up for modern businesses, Novo is 100% online, boasts absolutely no monthly fees, and carries no minimum balance requirements. Its interface is beautiful, intuitive, and works flawlessly on both desktop and mobile devices.

The biggest drawing card for Novo is its “Novo Reserves” feature. As a freelancer, remembering to save for taxes is a constant struggle. Novo allows you to create up to 20 Reserves (effectively digital envelopes). You can set auto-routing rules so that every time an invoice is paid, 25% automatically goes into your “Tax Reserve” and 10% goes into a “Profit Reserve.” This is essentially hands-free cash management.

Furthermore, Novo plays extremely well with the tech stack you likely already use. It has deep, native integrations with platforms like Stripe, Shopify, Wise, and QuickBooks. When a client pays a Stripe invoice, you see it reflected in your Novo dashboard much faster than with traditional banks.

- Best Feature: Seamless integration with Stripe, Shopify, and Wise.

- Pros: Excellent Reserve system for automated tax saving; user-friendly app; refunds ATM fees (up to $7/month); integrates with dozens of external tools.

- Cons: No cash deposits allowed; occasional delays in check clearing times.

- The 2026 Edge: Enhanced AI-driven cash flow forecasting that analyzes your past invoice data to help you predict your slow months and prepare accordingly.

2. Bluevine: Best for Earning High-Yield Interest

Why let your business cash sit idle when it could be working for you? Inflation doesn’t sleep, and keeping all your working capital in a 0.01% APY account is leaving money on the table. Enter Bluevine, a financial technology company that offers one of the highest interest rates in the commercial banking industry on your everyday operating funds.

Currently, Bluevine offers up to a staggering 2.0% APY on qualifying balances (up to $250,000). To qualify for this rate, you simply need to meet one of two easy criteria each month: either spend $500 on your Bluevine debit card, or receive $2,500 in customer payments. For most full-time freelancers, hitting these minimums is effortless.

Beyond the impressive yield, Bluevine acts more like a traditional bank than some of its fintech peers. It allows you to deposit cash at over 90,000 Green Dot locations (though a small fee applies per deposit), gives you two free checkbooks, and offers a straightforward line of credit application process if your business needs emergency capital to bridge a slow season.

- Best Feature: High-yield interest on your operating capital.

- Pros: Top-tier APY on checking; no monthly fees; allows cash deposits; provides physical checkbooks.

- Cons: Must meet activity requirements to earn the high interest rate; cash deposit fees at Green Dot locations.

- The 2026 Edge: Unlimited sub-accounts with their own dedicated account numbers, making it easier than ever to organize different revenue streams or separate specific client funds.

3. Relay: Best for “Profit First” Users & Growing Agencies

If you have read Mike Michalowicz’s phenomenal book Profit First and want to implement that cash management system, Relay is your absolute best friend. The Profit First method relies on moving your revenue into multiple, highly specific accounts (Income, Profit, Taxes, Owner’s Pay, Operating Expenses) as soon as it hits your bank.

Most traditional banks would charge you $15-$25 a month for each of those separate checking accounts. Relay allows you to open up to 20 individual, free checking accounts with zero monthly fees and no minimum balance requirements. It was practically designed for the Profit First methodology.

But Relay isn’t just for solo freelancers; it is built to scale with you if you plan on expanding into an agency. Relay allows you to issue up to 50 virtual and physical debit cards. If you hire a virtual assistant or a Facebook Ads contractor, you can issue them a specific card with strict spending limits. No more sharing your primary debit card number over Slack.

- Best Feature: Multiple checking accounts and up to 50 debit cards for granular budget control.

- Pros: Built-in integration with Profit First principles; incredible multi-user access permissions; extremely detailed transaction data.

- Cons: No cash deposits; the UI can feel slightly more complex due to the volume of features.

- The 2026 Edge: Deep integration with QuickBooks Online and Xero that matches transactions with 99.9% accuracy, eliminating the dreaded “uncategorized expense” pileup at the end of the year.

4. Found: Best for Simple Bookkeeping & Tax Automation

Found breaks the mold by being more than just a place to park your money. It is positioned as an all-in-one financial ecosystem specifically tailored for self-employed individuals who hate administrative chores. Found combines banking, bookkeeping, invoicing, and tax preparation into one centralized application.

When you get paid through a Found invoice (or a connected payment processor like Stripe), the app immediately calculates your estimated tax burden in real-time based on your tax profile. It automatically moves that exact amount into a locked Tax folder. You never even see it in your “available to spend” balance, which completely eliminates the temptation to spend the IRS’s money.

Every time you swipe your Found debit card, the app prompts you to categorize the expense and attach a photo of the receipt. By the end of the year, your Schedule C is essentially already filled out. For a freelancer who cannot afford a dedicated bookkeeper and dreads using complex accounting software, Found is a lifesaver.

- Best Feature: Automatic tax withholding and built-in professional invoicing.

- Pros: Streamlines bookkeeping; creates professional invoices directly from the app; incredible automated tax saving.

- Cons: Not ideal if you already pay for and prefer robust software like QuickBooks; fewer integrations with third-party apps compared to Novo.

- The 2026 Edge: One-click quarterly estimated tax payments sent directly to the IRS from the app’s dashboard—no need to navigate the clunky EFTPS government website.

5. Mercury: Best for Scaling Tech Freelancers & SaaS Creators

While Mercury is famously known as the bank for venture-backed Silicon Valley startups, it is an incredible tool for high-earning freelancers, software developers, and solo agency owners who need a premium, high-octane banking experience. If you process high-volume domestic or international wires, Mercury handles them better than almost any other free option on the market.

Mercury is completely fee-free—no monthly fees, no minimum balances, and remarkably, no fees on domestic or international wire transfers (a rarity in the banking world). The user interface is sleek, fast, and engineered to perfection. For tech-savvy freelancers, Mercury also offers read-write API access so you can build custom internal dashboards or automate your finance workflows.

If you are holding significant capital in your business from a recent software sale or large retainer deal, Mercury provides robust security and peace of mind, backing your funds with massive institutional partnerships.

- Best Feature: Free wire transfers (domestic and international) and world-class user interface with API access.

- Pros: Ideal for high-revenue solo businesses; excellent UI; top-tier security; virtual cards created instantly.

- Cons: Geared more toward incorporated entities (LLCs, C-Corps) than basic sole proprietors; no cash deposit capabilities.

- The 2026 Edge: “Mercury Vault” automatically sweeps overflow funds into a network of partner banks, providing massive FDIC insurance coverage up to $5 Million.

Having a dedicated business account makes it infinitely easier to fund your retirement as a freelancer. When your business operating cash, tax money, and personal spending money are decisively separated, you gain a crystal clear picture of your true profit. This allows you to confidently see exactly how much you can afford to contribute to your Fidelity Solo 401(k) or Traditional IRA without accidentally spending cash you meant to save for a rainy day.

Which Bank Account Should You Choose?

There is no “one size fits all” answer, but here is a quick framework to make your decision:

- If you want the most hands-off automation and hate accounting, open a Found account.

- If you hold a large cash balance and want the best interest yields, open a Bluevine account.

- If you want the most flexibility to run the Profit First system and grow into a larger agency, choose Relay.

- If you rely heavily on software tools like Shopify or Stripe and want great integrations, choose Novo.

- If you are a high-earning tech freelancer making international transfers, choose Mercury.

Ultimately, the most critical step isn’t picking the absolute “perfect” bank—it’s simply making the decision to open one today so you can immediately stop mixing your money. Once your free account is live and your finances are clearly separated, protect yourself further by reading our comprehensive guide on How to Pay Quarterly Taxes to stay off the IRS radar.

Frequently Asked Questions (FAQ)

Do freelancers actually need a business bank account?

Yes. While sole proprietors are technically allowed to use a personal account, it creates a massive accounting burden and makes audits difficult. If you operate as an LLC or S-Corp, a dedicated business bank account is legally required to maintain your limited liability protection and prevent “piercing the corporate veil.”

Can I open a business bank account with just my Social Security Number (SSN)?

Yes. If you operate as a sole proprietor and have not registered an LLC, you can open a business banking account using your SSN instead of an Employer Identification Number (EIN). Most modern fintech banks like Found, Novo, and Bluevine easily support sole proprietorship applications.

Will opening a business account impact my personal credit score?

Opening a standard business checking account typically requires a “soft pull” on your credit to verify your identity, which does not impact your credit score. Hard inquiries are only triggered if you apply for a business credit card or a line of credit through the bank.

What is the best way to pay myself as a freelancer from a business account?

The cleanest method is to set up a recurring ACH transfer (often called an Owner’s Draw) from your business checking account to your strictly personal checking account. Make sure you leave enough money in the business account to cover operating expenses and quarterly estimated taxes.

Are these online-only fintech banks completely safe for my money?

Yes, the platforms listed above partner with traditional banking institutions (like Middlesex Federal Savings or Evolve Bank & Trust) to hold your deposits. This means your money is FDIC-insured up to at least $250,000, just as it would be at a physical brick-and-mortar branch.