There is a terrifying moment in every successful freelancer’s career when they realize the stakes have gotten high. You are signing bigger contracts, handling sensitive client data, and taking on massive projects.

Suddenly, the thought creeps in: “What happens if I make a massive mistake and this client decides to sue me?”

Many 1099 contractors assume that simply existing as a freelancer means they fly under the radar of corporate lawsuits. Others think that having an LLC makes them completely bulletproof. Let’s break down exactly how freelance business insurance works in 2026, and whether or not you actually need to buy it.

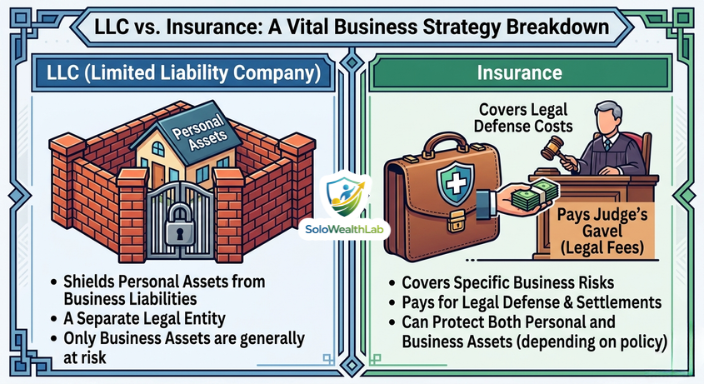

- An LLC Is Not Enough: Your LLC shields personal assets from lawsuits, but it does NOT pay your legal defense fees. Insurance does.

- E&O Is Non-Negotiable: Professional Liability (Errors & Omissions) insurance is the single most important policy for knowledge workers like designers, writers, and developers.

- Enterprise Clients Require It: Many large corporate clients will refuse to sign a contract with you unless you can provide a Certificate of Insurance (COI).

- It’s Surprisingly Affordable: Basic freelance insurance policies start at as little as $25–$40 per month from providers like Next Insurance and Hiscox.

In This Guide

- “But I Have an LLC! Isn’t That Enough?”

- 1. Professional Liability (Errors & Omissions)

- 2. General Liability Insurance

- 3. Cyber Liability Insurance

- 4. Business Owner’s Policy (BOP): The Bundle Deal

- 5. Who Actually Requires You to Have Insurance?

- 6. How to Buy Freelance Business Insurance in 2026

- The Final Verdict: Do You Need It?

- Frequently Asked Questions (FAQ)

“But I Have an LLC! Isn’t That Enough?”

This is the most common and dangerous misconception in the freelance world. Yes, an LLC is an incredible tool, but you need to understand exactly what it does and—just as critically—what it does not do.

An LLC is a corporate shield. If your business gets sued, the LLC prevents the client from coming after your personal assets, like your house, your car, or your personal savings. That protection is genuinely valuable and you should absolutely have one.

However, an LLC does not pay for your legal defense. If a client sues your LLC, you still have to hire a lawyer to defend the business. If your business bank account doesn’t have the $20,000 required to fight the lawsuit in court, your business goes bankrupt. Insurance pays the lawyers so your business survives.

Think of it this way: an LLC is a fireproof safe protecting your personal valuables. Insurance is the fire department that actually comes to put out the blaze. You need both.

Before you even think about buying insurance premiums, make sure your legal foundation is actually locked in. Read our guide: Protect Your Assets: Sole Proprietor vs. LLC for Freelancers (2026) to see if you need to file state paperwork first.

1. Professional Liability (Errors & Omissions)

Also known as E&O insurance, this is the absolute most important coverage for knowledge workers. If you are a freelance writer, graphic designer, web developer, marketing consultant, photographer, or financial advisor, Professional Liability insurance is the one policy you cannot afford to skip.

The fundamental risk of being a knowledge worker is that your work product—your words, your code, your strategy—directly influences your client’s business outcomes. When something goes wrong, and sometimes it will, clients will look for someone to blame and someone to pay.

- What it covers: It protects you if a client claims your work was inaccurate, delivered late, failed to perform as promised, or caused them to lose money. It covers both the legal defense costs and any resulting settlement or judgment.

- What it does NOT cover: Intentional fraud, physical injuries, or property damage. Those fall under different policies.

- The 2026 Scenario: You are a freelance web developer, and you accidentally introduce a bug that crashes a client’s e-commerce site on Black Friday. The client loses $50,000 in sales and sues you for the damages. E&O insurance covers the legal fees and the settlement, so the mistake doesn’t end your entire business.

For most service-based freelancers, E&O coverage of $1 million per occurrence is the standard baseline that enterprise clients will expect to see on your Certificate of Insurance.

2. General Liability Insurance

This is the original “slip and fall” insurance that has existed for decades. While it is most commonly associated with physical businesses like restaurants and retail stores, it is also highly relevant if you interact with clients in person, rent a coworking space, attend on-site shoots or events, or handle any client-owned physical property.

- What it covers: Physical bodily injury, third-party property damage, and sometimes advertising injuries such as accidental copyright infringement in your marketing materials.

- The 2026 Scenario: You are a freelance videographer filming a corporate commercial. The CEO trips over your lighting equipment cord, breaks their arm, and demands you cover their $15,000 in medical bills and lost income. General Liability steps in to cover the costs before they escalate into a full lawsuit.

Even if you work entirely from home and never meet clients in person, many commercial landlords and coworking space memberships require proof of General Liability coverage before allowing you to sign a lease. It is the cost of doing business in a physical world.

3. Cyber Liability Insurance (The Modern Necessity)

If you handle sensitive client data of any kind—customer email lists, login credentials, financial records, healthcare information, or proprietary business strategies—Cyber Liability insurance is becoming a non-negotiable reality in 2026.

The threat landscape has escalated dramatically. Freelancers are increasingly targeted by ransomware attacks because they tend to have weaker security infrastructure than the large corporations they serve. A single successful phishing attack can expose thousands of your client’s customers, and the recovery process is enormously expensive.

- What it covers: Data breach notification costs (legally required in most states), forensic investigation services, data recovery expenses, business interruption losses, ransomware payments, and third-party liability if affected customers sue your client because of your breach.

- The 2026 Scenario: Your laptop is stolen from a coffee shop. It contained a client’s entire CRM database of 15,000 customer records. You are now legally required to hire a breach notification firm, notify all 15,000 people by mail, and potentially offer them identity monitoring for 12 months. Cyber Liability pays those bills.

4. Business Owner’s Policy (BOP): The Bundle Deal

A Business Owner’s Policy (BOP) is essentially a bundled insurance package that combines General Liability coverage and Commercial Property insurance into a single, discounted policy. Insurers offer BOPs specifically to small business owners who need multiple forms of basic protection without paying separately for each.

If you own significant business equipment—an expensive camera setup, a high-end workstation, professional audio gear, or even a dedicated office space filled with furniture—a BOP is usually more cost-effective than purchasing individual policies.

- What it covers: General Liability claims (bodily injury, property damage) PLUS physical protection for your own business equipment and property against theft, fire, or vandalism.

- Who needs it most: Freelance photographers, videographers, audio engineers, or any creative professional with thousands of dollars of gear whose destruction would halt their entire business overnight.

Most providers can upgrade a BOP with additional riders, allowing you to add E&O or Cyber Liability coverage on top of the base bundle for a modest premium increase. Always ask your insurer about bundling discounts before purchasing coverage piecemeal.

5. Who Actually Requires You to Have Insurance?

One of the most compelling reasons to buy freelance business insurance in 2026 has nothing to do with your own risk tolerance. The market itself is increasingly requiring it as a baseline condition of doing business.

Here is exactly who will ask for your Certificate of Insurance (COI) before signing with you:

- Enterprise and Fortune 500 clients: Most large corporations have strict vendor compliance requirements. Their procurement teams routinely require $1 million or more in General Liability and E&O coverage before onboarding any external contractor, no matter how small.

- Government contracts: Any freelance work on a municipal, state, or federal government project will almost universally require proof of insurance as a legal prerequisite to signing the service agreement.

- Agencies who subcontract work to you: Marketing agencies, PR firms, and production companies who bring you in as a 1099 subcontractor often require their subs to carry their own insurance so the agency is not responsible for your mistakes.

- Coworking spaces and commercial landlords: Even basic shared workspace memberships in many cities now require General Liability proof upon signing the membership agreement.

The moment you start targeting premium clients with larger budgets, you will find that insurance stops being optional. It becomes a literal hard requirement for accessing that level of business.

6. How to Buy Freelance Business Insurance in 2026

The insurance-buying process has been dramatically modernized. Gone are the days of sitting down with a local agent for hours to fill out paper applications. In 2026, the best freelance insurance providers offer fully online applications that produce real quotes in under 10 minutes.

Here are the top providers purpose-built for freelancers and independent contractors:

- Next Insurance: Widely considered the best digital-first insurer for small businesses. Their entire process is online, certificates are issued instantly, and you can adjust coverage on a monthly basis without penalties. Starting at around $25/month for basic General Liability.

- Hiscox: One of the oldest and most reputable specialty insurers for small businesses and knowledge workers in particular. Extremely strong E&O policies for consultants, designers, and developers. Policies start at roughly $30–$40/month.

- Thimble: The best option if you need temporary, project-based coverage rather than an annual policy. You can literally purchase insurance by the hour, day, or week for a specific gig, making it extremely cost-effective for occasional freelancers.

- Simply Business: An insurance marketplace that pulls quotes from multiple carriers simultaneously, allowing you to compare options side-by-side without filling out separate applications for each provider.

When applying, you will be asked to provide your business name, your profession, your annual estimated revenue, and how many employees or subcontractors you work with. Be honest and accurate—misrepresenting your business profile can invalidate a claim when you need it most.

Insurance is one piece of your freelance financial armor. Make sure the rest of your back-office is bulletproof too. Read our guide to the 5 Best Free Business Bank Accounts for Freelancers to keep your personal and business finances legally separated, and check out our Best Invoicing & Bookkeeping Tools to make sure every dollar is tracked and every deduction is captured at tax time.

The Final Verdict: Do You Need It?

If you are making $500 a month writing occasional blog posts for two small clients and your contracts are informal verbal agreements, you can likely skip purchasing insurance for now. The risk profile simply isn’t there yet.

However, if freelancing is your full-time career and primary income source, you are signing written contracts worth $5,000 or more per project, you handle any client data or produce deliverables that directly impact their revenue, or your target client roster includes enterprise companies, agencies, or government entities—you absolutely need a policy. This is not optional risk management; it is a business continuity strategy.

Most modern providers like Next Insurance or Hiscox offer basic freelance policies for as little as $25 to $40 a month. That is less than a Netflix subscription and a single cup of specialty coffee per week. It is a negligibly small price to ensure that one difficult client, one overlooked bug, or one stolen laptop does not wipe out everything you have spent years building.

Get the coverage. Protect the business.

Frequently Asked Questions (FAQ)

Is freelance business insurance tax deductible?

Yes. Business insurance premiums paid to protect your freelance operation are fully deductible as an ordinary and necessary business expense on Schedule C of your federal tax return. This means if you are in the 22% tax bracket and pay $480 per year in premiums, your effective out-of-pocket cost after the deduction is closer to $374. Always confirm specific deductions with your CPA.

Do I need insurance if I work from home and never meet clients?

Possibly yes, but for different reasons than you might think. If you handle client data digitally, Cyber Liability is still highly relevant. If you target enterprise or agency clients, they will require a Certificate of Insurance regardless of your physical work location. And if a deliverable you produce causes financial harm to a client, Professional Liability (E&O) coverage still applies even if the work was done entirely remotely.

What is a Certificate of Insurance (COI) and why do clients ask for it?

A Certificate of Insurance (COI) is a one-page document issued by your insurer that summarizes your coverage types, policy limits, and effective dates. Clients request it to verify that you are actually insured and that your policy limits meet their vendor compliance requirements. Your insurer can generate and email a COI in minutes at no extra charge, typically through your online account portal.

How much does freelance business insurance typically cost?

For most freelancers, a basic General Liability policy with $1 million per occurrence coverage costs between $25 and $50 per month. Adding Professional Liability (E&O) typically brings the total to $50–$100 per month depending on your profession and annual revenue. High-revenue consultants (over $500,000 annually) or those in regulated industries like finance or healthcare may see higher rates.

Does my LLC protect me from everything, making insurance unnecessary?

No. An LLC shields your personal assets from business debts and lawsuits, but it does not pay your legal defense costs. Even a frivolous lawsuit that you ultimately win can cost $15,000 to $50,000 in attorney fees. If your LLC’s bank account cannot absorb those costs, your business becomes insolvent. Insurance pays the lawyers and any settlements so that your LLC—and your income—survives the fight.