- If you expect to owe more than $1,000 in self-employment and income taxes, you must pay quarterly.

- Failing to meet IRS deadlines (April 15, June 15, Sept 15, Jan 15) triggers underpayment penalties and compounding interest.

- Use the “Safe Harbor Rule” (paying 100% of last year’s tax liability) to guarantee you are immune from underpayment penalties.

- Freelancers must account for both standard income tax and the 15.3% self-employment tax when calculating their burden.

- Make your payments directly online via the IRS Direct Pay portal, rather than mailing a physical check.

The Tax Shock of Freelancing

One of the biggest shocks for new freelancers, gig workers, and solopreneurs is the very first tax season. When you work a standard W-2 corporate job, your employer magically withholds taxes from every paycheck. You never even see the money. The accounting department does the heavy lifting, sending fractions of your salary to the federal and state governments before your direct deposit clears your bank account.

When you are self-employed, you are the employer and the employee. You are entirely responsible for paying those taxes yourself. The government has no direct line into your checking account to siphon off its share, so the burden of estimating and remitting those funds falls entirely on your shoulders. If you wait until April of the following year to pay your entire tax bill in one giant lump sum, the IRS is going to hit you with a massive underpayment penalty.

To avoid this stressful scenario, you need to understand how quarterly estimated taxes work. Getting your head around quarterly estimated taxes freelancer requirements sounds incredibly intimidating when you are first starting out, but once you set up a reliable system, it takes less than 15 minutes every few months. Here is your ultimate 2026 guide to calculating, tracking, and paying your freelance taxes without the headaches.

What Are Quarterly Estimated Taxes?

The United States tax system operates on a “pay-as-you-go” basis. The IRS expects to receive a cut of your income as you earn it throughout the year, not all at once at the bitter end. As a 1099 contractor, gig economy worker, or small business owner, your quarterly estimated tax payments are designed to cover two distinct categories of tax liability:

- Income Tax: Your standard federal and state income taxes, which are dictated by your overall tax bracket. This is the same tax W-2 employees pay, sliding up incrementally based on how much net profit you make across the year.

- Self-Employment Tax: This is a flat 15.3% federal tax that covers your mandatory Medicare and Social Security contributions. When you work a W-2 job, your employer pays 7.65% and you pay the other 7.65%. Because you are self-employed, you owe the entire 15.3% yourself.

Because nobody is withholding these two chunks of money for you, the IRS demands that you send in a “best guess” estimate four times a year. If you fail to make these ongoing deposits, the IRS essentially views it as an unauthorized zero-interest loan you took from them, and they will retaliate with costly penalties.

Do I Actually Have to Pay Them?

If you’ve recently transitioned from a W-2 role to a freelance role, you might be wondering if you truly fall under this mandate. The IRS rule is relatively simple and explicitly defined:

If you expect to owe $1,000 or more in federal taxes for the 2026 tax year—after subtracting any W-2 withholding (if you still hold a part-time job) and refundable tax credits—you must make estimated quarterly tax payments.

For most full-time freelancers, agency contractors, and busy gig economy workers (like full-time Uber drivers, Upwork specialists, or Airbnb hosts), you will cross this $1,000 threshold extremely quickly. Earning just a few thousand dollars in net 1099 profit will easily trigger enough self-employment tax to force you over the limit. When in doubt, it is far safer to pay quarterly and receive a refund later rather than skipping payments and risking IRS penalties and compounded interest later.

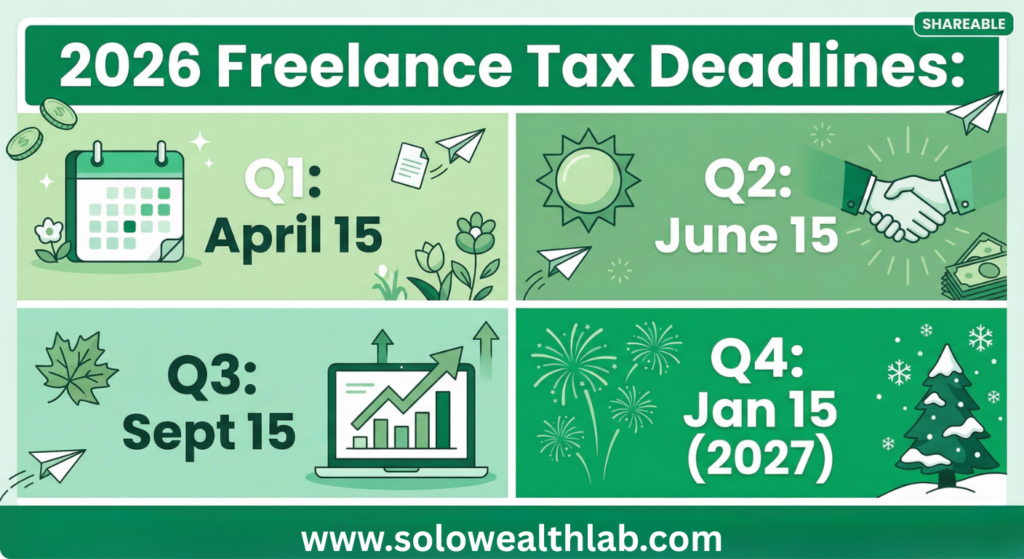

The 2026 IRS Deadlines

The IRS stubbornly divides the calendar year into four payment periods that do not align perfectly with standard 3-month corporate quarters. It is imperative that you mark these exact dates on your 2026 calendar, put reminders on your phone, and treat them as non-negotiable. If you miss them, you will accrue penalties and interest.

- Q1 Payment (Income earned Jan 1 – Mar 31): Due April 15, 2026

- Q2 Payment (Income earned Apr 1 – May 31): Due June 15, 2026

- Q3 Payment (Income earned Jun 1 – Aug 31): Due September 15, 2026

- Q4 Payment (Income earned Sep 1 – Dec 31): Due January 15, 2027

Note: If a deadline falls on a weekend or a federal holiday (like Emancipation Day in Washington D.C.), the deadline automatically shifts to the next immediate business day.

How to Calculate What You Owe

Calculating your exact tax burden can feel overwhelming because freelance income often fluctuates wildly. One month you might make $10,000, and the next month you make $2,000. How do you estimate taxes on a moving target? Here are the two best, stress-free ways to handle the math:

The “Safe Harbor” Rule (The IRS-Proof Method)

If your business is established and you want an absolute mathematical guarantee that you will never get hit with an underpayment penalty, you should leverage the Safe Harbor rule. The IRS allows you to sidestep the requirement of perfectly predicting your current year’s income.

Instead, you pull up your tax return from last year, look at your “Total Tax” line, and simply divide that exact number by four. As long as you pay 100% of the total tax you owed last year (or 110% if your Adjusted Gross Income was over $150,000 for married filing jointly or $75,000 for singles), you are fully protected from penalties—even if your business suddenly skyrockets and you make triple the amount of money this year.

You will still owe the remaining balance of the tax next April, but the government won’t punish you with late fees for under-estimating.

The 30% Rule (The Beginner Method)

If this is your first year freelancing, you do not have a previous freelance tax return to base your “Safe Harbor” payments on. In this scenario, guessing your tax bracket requires discipline.

A proven rule of thumb is to open a separate, high-yield business savings account. Every single time a client pays an invoice or you receive a payout from an app, instantly and automatically transfer 25% to 30% of that gross payment directly into the tax savings account. Do not touch this money for operating expenses or personal bills. It is no longer yours; it belongs to the federal government. When the quarterly deadline arrives, log onto the IRS portal and send all the cash accumulated in that bucket.

This method prevents you from scrambling to find thousands of dollars at the end of the quarter. By removing the funds immediately from your checking account, you build forced scarcity and learn to survive on your actual after-tax profit.

Don’t Forget: State Estimated Taxes

A fatal mistake made by countless new freelancers is meticulously calculating and paying their federal IRS taxes while entirely forgetting about their home state’s Department of Revenue. State governments want their money quarterly as well.

If you live in a state that levies income taxes (such as California, New York, or Illinois), you must make simultaneous scheduled estimated payments to your state’s tax agency. Fortunately, their deadlines almost always mirror the IRS federal deadlines listed above. Just remember that you will need to log into two separate portals on those four critical days.

(If you live in a state with no income tax, like Texas, Florida, or Nevada, you only have to worry about federal IRS payments.)

How to Actually Pay the IRS

In modern 2026, there is zero reason to rely on the unpredictable U.S. Postal Service and physical paper checks to satisfy a government mandate. The easiest, fastest, and most secure way to pay your quarterly taxes is directly online via ACH transfer.

- Go directly to the official IRS Direct Pay portal.

- Click on “Make a Payment.”

- In the dropdown menu for “Reason for Payment,” correctly select Estimated Tax.

- Apply the payment to the current tax year (Select 2026).

- Verify your identity by providing information from a previous tax return.

- Enter your business checking account routing and account numbers, and hit submit.

Alternatively, if you are incorporated as an S-Corp or prefer advanced scheduling, you can register for the EFTPS (Electronic Federal Tax Payment System). EFTPS allows you to queue up all four payments months in advance so they automatically pull from your bank on the exact deadline day.

The best way to owe the IRS less money every quarter is to aggressively claim your legal 1099 business write-offs before calculating your net profit. Check out our Top 5 Gig Economy Tax Strategies for 2026 to see how the new 72.5-cent mileage rates and permanent QBI deductions can drastically slash your tax bill.

What If My Income Fluctuates Wildly?

Freelance life means feast or famine. What happens if you pay a massive sum for Q1 based on an incredible month, but your Q2 income plummets to near zero? Do you still have to send a huge payment?

No. If your income drops significantly, simply lower your next estimated payment to align with your newly diminished expectations using an Annualized Income Installment Method form. Remember, estimated taxes are an ongoing conversation with the IRS. If you massively overpay early in the year, the IRS will simply refund you the surplus when you file your official Form 1040 next April. However, adjusting your rate downwards preserves your cash flow during a freelance dry spell.

Frequently Asked Questions (FAQs)

What happens if I miss a quarterly tax deadline?

If you miss a quarterly estimated tax deadline, the IRS will calculate an underpayment penalty based on the exact number of days your payment was late, multiplied by a federally set interest rate short-term. To minimize the damage, log in and make the payment as soon as possible rather than waiting to bundle it with the next quarter’s deadline.

Can I just pay all my freelance taxes at the end of the year?

No. The United States operates on a mandatory pay-as-you-go tax system. By law, if you expect to owe more than $1,000 in your 1099 role, you are legally obligated to make quarterly payments. Waiting until April to clear an entire year’s worth of earnings will trigger substantial, unnecessary underpayment penalties and fees.

How does the IRS Safe Harbor rule work?

The Safe Harbor rule is a protection mechanism. It mathematically guarantees you will not face penalties if you pay 100% of your prior year’s total tax liability (or 110% if your AGI was over $150,000) over four equal quarterly installments. This shields you from penalty risk completely, regardless of how much your business scales in the current year.

Do I have to pay both federal and state estimated taxes?

Yes. If your state levies an individual income tax, you generally must make simultaneous quarterly estimated tax payments to your state’s Department of Revenue. State deadlines usually copy the same four federal dates, but you must make the payment through a separate state-owned web portal.

What percentage of my freelance income should I save for taxes?

Tax brackets differ, but tax professionals universally recommend that freelancers and independent contractors divert 25% to 30% of their gross payout into an untouchable high-yield savings account. This conservative buffer guarantees you have enough liquidity to cover your 15.3% self-employment burden alongside standard income taxes.

Conclusion & Next Steps

Transitioning from the safe comfort of a W-2 salary to the unpredictable, liberating landscape of freelancing requires you to quickly master new financial habits. Paying quarterly estimated taxes is arguably the most critical habit to establish early in your solopreneur journey.

Do not let the fear of IRS penalties freeze your business growth. Use an automated accounting tool like QuickBooks Self-Employed or FreshBooks to easily track your income, immediately scrape 30% of every payment into a segregated tax vault, and simply hit “pay” four times a year on the IRS Direct Pay site. By treating your quarterly tax obligations as standard, manageable business overhead, you remove the stress from tax season and protect the cash flow of your growing freelance enterprise.